A Complete Guide to IRS Private Collection Agencies and Your Rights

Private collection agencies (PCAs) have become a regular part of the IRS’s strategy for collecting overdue tax debts, but their history is anything but smooth. From failed attempts in the past to renewed success under new laws and taxpayer protections, the relationship between the IRS and these private agencies has evolved significantly. Understanding how PCAs operate, who they are, and what your rights are if they contact you can help you avoid scams and take control of your tax situation with confidence.

Key Takeaways

Private collection agencies now assist the IRS in recovering old tax debts under updated laws.

The Taxpayer First Act added strong protections for low-income taxpayers and extended repayment options.

You can legally request that a PCA stop contacting you and return your account to the IRS.

A Little Background on Private Collection Agencies

Private Collection Agencies (or PCAs) aren’t new to the IRS’s world of tax-debt collection. In fact, they’ve been brought in a few times before — first in the late 1990s, then again in the mid-2000s. But those early attempts didn’t go so well. The agencies cost more money than they brought in and created unfair situations for some taxpayers, so the programs were eventually shut down.

Even so, history repeated itself in 2015 when Congress passed the Fixing America’s Surface Transportation (FAST) Act. It might sound like a highway bill (and it is), but tucked inside was a rule that required the IRS to use PCAs again — this time to collect on older tax debts that the IRS had stopped pursuing directly.

Protecting Taxpayers

After some well-deserved criticism, lawmakers made sure to add new safeguards. In 2019, Congress passed the Taxpayer First Act (TFA) to give low-income taxpayers more protection. Under this law, the IRS can’t assign a case to a private collection agency if the taxpayer’s income is less than 200% of the federal poverty level — roughly $32,150 for a family of four in 2025.

The TFA also changed the rules about when a PCA can get involved. Now, the debt has to be at least two years old before a private collector can take it on (it used to be just one year). Plus, taxpayers working with a PCA can now stretch out their installment payments for up to seven years instead of the previous five — a small but meaningful bit of breathing room.

How Things Are Going Now

Although earlier programs flopped financially, the latest round has seen more success. Between 2017 and 2021, the IRS handed off around 4 million delinquent accounts to PCAs. Those agencies brought in more than $1 billion in commissionable payments and another $68.7 million in non-commissionable ones — a sign that, this time around, the partnership is at least paying off.

Which PCAs Work With The IRS

Currently, the IRS is contracted to work with the following three private collection agencies:

| CBE Group Inc. P.O. Box 2217 Waterloo, IA 50704 800-910-5837 | Coast Professional, Inc. P.O. Box 7425 Geneseo, NY 14454 888-928-0510 | ConServe P.O. Box 307 Fairport, NY 14450 844-853-4875 |

If you receive a call or text from someone claiming to be from an IRS private collection agency, do not provide any information unless they are from one of these businesses. You should never be contacted out of the blue. The IRS and PCAs must follow certain steps when assigning your tax debt to collections.

How It Works

Before a PCA can contact you by phone or text, you will receive two letters.

- IRS Notice CP40. This notifies you that your tax debt was assigned to a private collection agency.

- Initial contact letter. This letter is from the assigned PCA and outlines information on how to resolve your tax debt.

Both of these letters will contain a taxpayer authentication number, which is used to confirm your identity.

What to Expect After Receiving a PCA Notice

After you receive the initial contact letter from the private collection agency, the PCA will contact you by phone to gather additional information. To ensure your information is safeguarded:

- Validate that the caller is from one of the three PCAs listed.

- Ask them to provide your taxpayer authentication number. If they do not have this or give the wrong number, hang up – they could be scammers!

Once you’ve verified that the caller is working with a legitimate PCA, you’ll be asked a series of questions so they can also verify your identity. They will also work with you to resolve your tax debt. Although they have the authority to negotiate repayment of your tax debt, payments should never go directly to the PCA. Checks should only be made payable to the U.S. Treasury and sent to the IRS.

The representative should be courteous, professional, and respect your taxpayer rights. If at any time you feel threatened or believe the PCA acted inappropriately, you can file a complaint with the U.S. Treasury Inspector General.

Are Taxpayers Required to Work With a PCA?

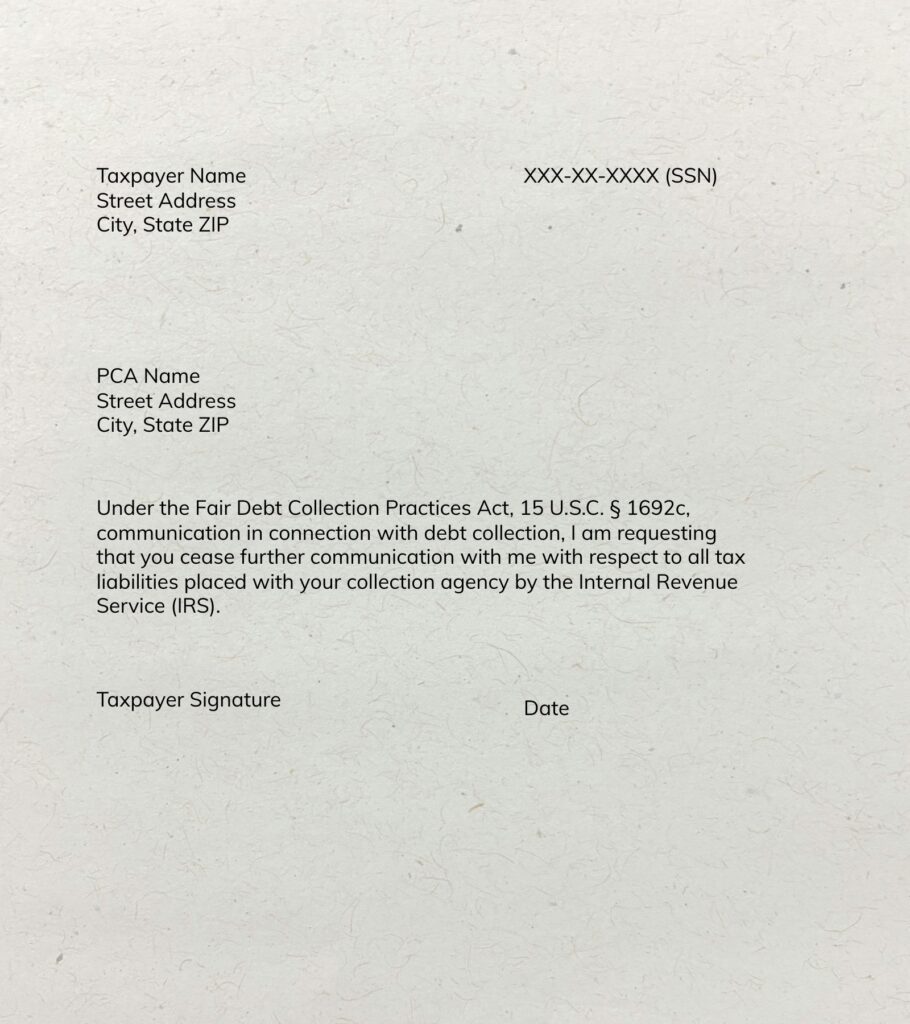

You might be surprised to learn that under 15 U.S.C. § 1692c (Fair Debt Collection Act), you have the right to demand that a private collection agency stop contacting you. If you prefer to work directly with the IRS to settle your tax debt, send a no-contact letter (see example below) to the PCA asking them to cease all contact at once. After they receive the letter, your account will be returned to the IRS.

Sample No-Contact Letter

Need Help?

If you’ve received a letter from a private collection agency, we strongly recommend speaking with a qualified tax professional to learn more about your tax resolution options. For a free consultation, give us a call today!